In the face of mortgage rates reaching 20-year highs, California homeowners find themselves at a crossroads. With record levels of home equity, many are opting to stay in their current homes to maintain low mortgage rates (~3%!) vs. the dreaded cost of selling and rebuying at 7-8%. This trend has created significant market dislocation in new home sales and in the second-mortgage space, affecting both home equity loans and Home Equity Lines of Credit (HELOCs).

With HELOC rates often soaring above 10% (for those who can secure them at all), and major financial institutions like Wells Fargo halting new HELOC applications, homeowners are in a bind. Wells Fargo’s HELOC page, for example, plainly states that they’ve given up, saying that “due to current market conditions, we are temporarily suspending new applications for home equity lines of credit.” It echoes a broader question: How do homeowners tap into their near-record equity when traditional methods become costly or unavailable?

Fortunately, as they say, necessity is the mother of (financial) innovation. Enter two new ways of accessing home equity without traditional debt, and without selling your home: home equity sharing / home equity investment (“HEI”) programs, and innovative programs from companies like Yardsworth, which buys a small piece of your yard for cash, allowing you to access hundreds of thousands of dollars of cash debt-free, tax-free, and without having to refi or move.

Both HEI programs and Yardsworth’s unique “yard purchase” program offer three key benefits vs. homeowners’ traditional options (namely, selling their home to access 100% of the equity, or borrowing against home equity with a HELOC or home equity loan):

- You keep your house: unlike selling your home and rebuying, HEI programs and selling your backyard to Yardsworth allow you to keep your house, and stay in your home/community

- You keep your low-rate mortgage: selling your home and moving to a new (lower-priced) area was historically the obvious way to tap home equity. House worth $750k and you have a $500k loan? Sell your home, pay ~$50k of commissions and expenses, and net $200k to buy a home across town. But, today, you’d need to trade in your 3% mortgage for a new 7-8%+ loan on a new home. Not worth it. Plus you love your home (and that low-rate mortgage)!

- You don’t increase your monthly debt burden: One of the promises of home equity sharing programs is that they give you cash “without additional debt.” This has always sounded great, but is even more compelling in today’s high-interest-rate mortgage environment. Who wants (or can afford) additional payments every month? Unfortunately, while they don’t require monthly payments, it’s still not entirely fair to say that HEI programs are “debt-free.” In fact, the legal agreements employed by many home-sharing programs look a lot like traditional second-lien (mortgage) contracts. In fact, they typically even have a 10- to 30-year term (just like a mortgage) during which you need to either sell your home or refinance to repay them… Sounds like debt to me, with the only benefit being that you don’t have monthly payments. Fortunately, Yardsworth’s cash payments to homeowners offer a truly debt-free solution.

Pros of Partnering with Yardsworth:

Immediate Financial Gain: Yardsworth pays homeowners a $100-200,000+ cash lump sum for the sale of part of their backyard space. You keep your house, keep your low-rate mortgage, and get debt-free cash. You just give up a small portion of your (probably unused) backyard. Retain Low Mortgage Rates: Homeowners working with Yardsworth can access their equity while retaining their current low mortgage rates, bypassing the need to refinance at higher rates or secure a second mortgage at double-digit interest rates. We encourage you to keep that 3% mortgage for as long as you can. Yardsworth works with your current lender to get their approval of the transaction. Your mortgage rate and monthly payment do not change. Contribute to the Housing Solution: By selling part of your yard space to Yardsworth, you’re contributing to the much-needed creation of new housing in California, benefiting the broader community. This worthwhile goal is why California passed SB-9 (the “HOME Act”) in 2022 to begin with – allowing homeowners to split off and sell part of their land, and enabling housing creation. By working with Yardsworth and remaining in your home and in your community, you’re helping to solve CA’s housing crisis (and getting 6-figures of cash). Yardsworth Increases Your Net Worth – it isn’t just “debt masquerading as equity”: HEIs can come with intricate and dense contracts, and they sound like a great deal at first blush. But, dig into that fine print and they can look more like high-interest rate debt. Yardsworth’s debt-free solution actually increases your net worth by working with the local government to up-zone your lot for its “highest and best use.” What does that mean in plain English? Yardsworth helps you carve off a piece of your backyard into a brand new lot, with a separate parcel number (APN), address, utilities, fence, and parking, and use it to build a small house or rental. That’s worth a lot more than a patch of dirt and flowers. Quick math on a hypothetical Yardsworth SB-9 lot split deal: Yardsworth pays you ~$150k in cash, covers 100% of all fees and expenses involved, your house gets re-appraised at a slightly lower value (say, down $50k) due to the smaller lot size, and you are immediately $100,000 richer ($150k cash – $50k home value = $100,000 net worth increase). You’re richer, have more cash in the bank, kept your low-rate mortgage, and didn’t take on any new debt.Cons of Home Equity Investments (HEIs):

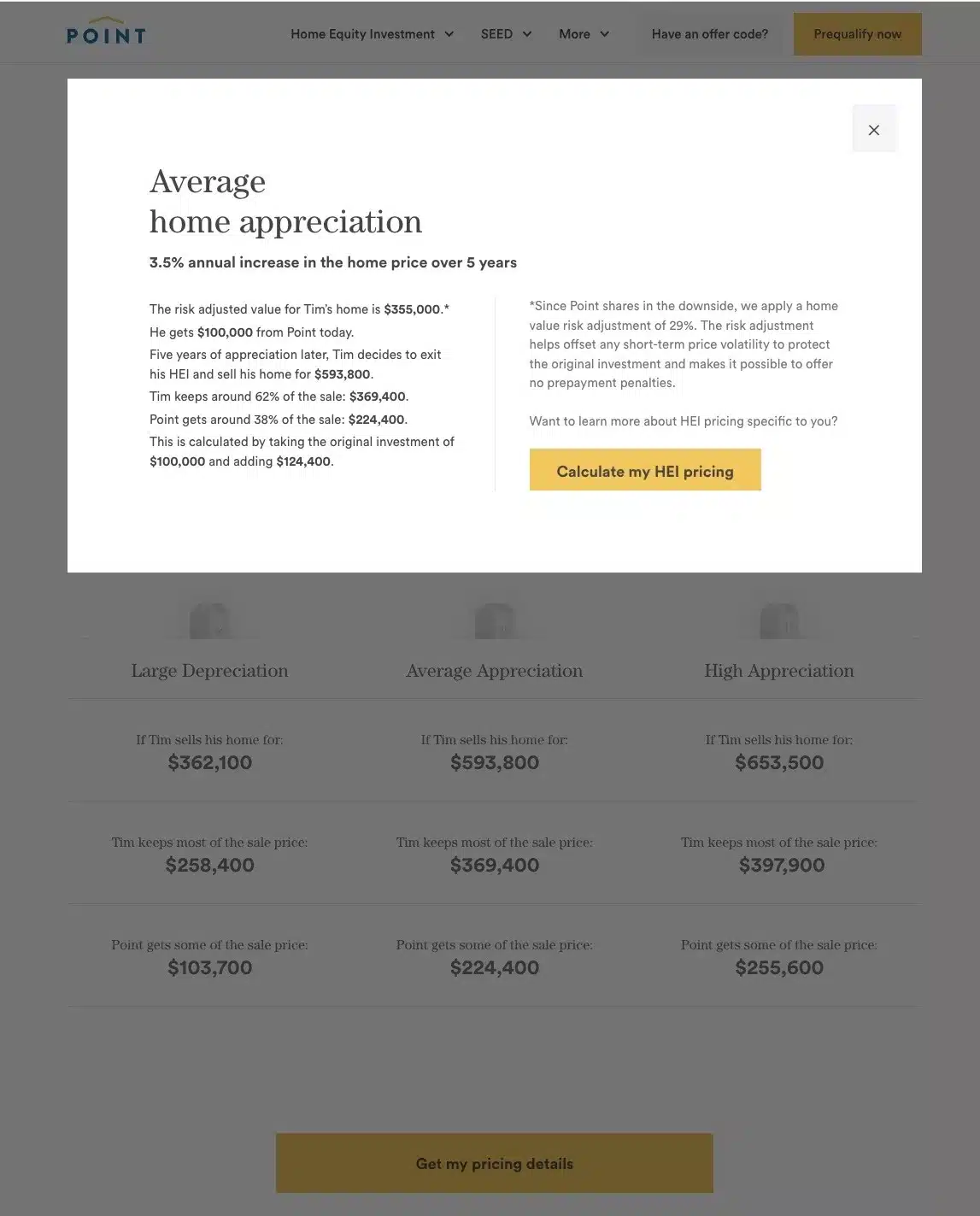

Some of the Most Expensive Cash You Can Find: Homeowners turn to home equity sharing programs because they don’t want to take on more debt, or simply can’t afford/stomach a HELOC at today’s ~10% second-mortgage rates. But, how much are you paying home equity sharing companies for that “debt-free” cash? The implied interest rates of HEIs can be shocking high. Point (no affiliation) is a home-sharing leader, and posted three examples on their website (first week of November, 2023) that make the case, as seen below.- First, HEI companies typically “haircut” (slash) the value of your home before investing. In the screenshot below, Competitor P notes that it applies a 29% discount (“risk adjustment”) to the value of “Tim’s” home before they invest. Do you really want to sell even a piece of your equity at a 29% discount?

- Second, the example below for “Tim” shows how much HEI companies receive even under base-case or “average home appreciation” scenarios. Let’s look at the math. Competitor P gives Tim $100,000 today, and assumes he sells his home after 5 years. What does “Time” owe Competitor P in return for his “equity sharing” agreement? He pays them back $224,400. That’s the equivalent of a 17.5% interest rate on a five-year loan! Who would knowingly agree to that? (quick math: ($224,400/$100,000)^(1/5)-1).

Profit Sharing: When selling equity to home equity sharing company, you agree to share future home value appreciation – this is why the effective interest rate you are paying on your “loan” can increase alongside your home value. Plus you are typically immediately locking in a huge discount (29% in the example above), ensuring the field is always tilted in the HEI company’s favor from the get-go. It’s a short-sighted trade, in many cases. Financial Complexity: Navigating HEI agreements can be daunting due to their intricate contracts and the long-term financial implications for homeowners. Do you really want to sign up to a 30-year agreement that limits your ability to keep your home forever, give it to your kids when the mortgage is paid off, or even refinance / borrow against it in the future? 30 years is a long time, and being required to sell your house or move isn’t something most people would choose to do. Yardsworth’s agreements are one-and-done. They pay you, and you have a new neighbor. And your house is yours, forever.Source: www.point.com/hei (screenshot as of 11/6/2023)